As a shareholder, understanding the details surrounding dividends is not just beneficial but essential for making informed decisions regarding your investments. For directors, a profound understanding of the legal considerations surrounding dividends is imperative, as it not only helps in avoiding potential liability but also ensures strict compliance with the law.

What are dividends?

When you subscribe for shares, you are not just acquiring a piece of a company, you are gaining a bundle of rights. These rights may include voting, the potential to reclaim your capital upon winding-up, and dividend. Dividends, simply put, are distributions of a company’s post-tax profits to its shareholders. It can either be in cash or in specie. Specie refers to the distribution`s physical or actual form, which can be for example property.

The golden rule regarding dividends, is set out in section 830 of the Companies Act 2006 (“CA 2006”), which asserts that dividends may only be paid out of distributable profits, as set out in the relevant accounts.

What are the different types of dividends?

Companies employ two main types of dividends – final and interim. The final dividend, typically paid once a year, follows a detailed process. After the annual accounts are prepared, the board recommends the final dividend, which shareholders then approve through an ordinary resolution. This resolution requires more than 50% of the shareholders present and voting at a live meeting. Once approved, the final dividend becomes a debt owed to the shareholder.

In contrast, interim dividends can be paid at any time and are generally smaller than a final dividend. Think of them as a ‘draw-down’ based on an estimate of the final dividend. The process is very simple, and the board only needs to declare the interim dividend. However, it’s important to note that interim dividends are not debts owed to shareholders and can be revoked.

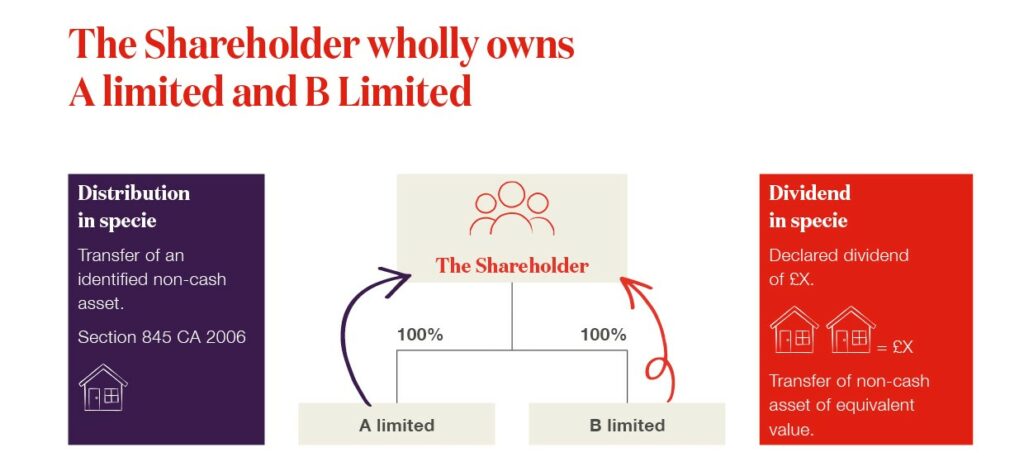

Dividends in specie and distribution in specie

To better understand dividends, we turn to the complexities of dividends in specie and distribution in specie:

What is dividend in specie?

This occurs when a dividend is declared in a cash amount but is satisfied by transferring assets of equivalent value. Adherence to the company’s articles of association (“articles”), especially Article 34 of the Model articles for private limited companies, is crucial when declaring a dividend in specie. The rules regarding distributable reserves still apply as mentioned below. Indicated in the diagram below in blue, a dividend was declared of £X but was satisfied by transferring non-cash assets of equivalent value.

What is distribution in specie?

Unlike dividend in specie, distribution in specie doesn’t require a prior declaration in cash as stated in section 845 CA 2006. It’s when a company makes a distribution of an identified non-cash asset without initially declaring an amount in cash. A transfer of an asset below market value result in the amount of the undervalue being considered as a distribution of specie. The rules regarding distributable reserves still apply. As noted in the diagram in orange, the asset was transferred without declaring same in cash.

(Diagram: The Shareholder wholly owns A limited and B Limited.)

What are the legal considerations when declaring dividends?

The declaration of dividends entails not only specifying the recipients, timing, and payment method but also involves significant legal considerations to avoid pitfalls and ensure compliance. Key legal considerations include:

- Amount: Verifying whether the company possesses enough distributable reserves (profits) to cover the intended distributions.

- Relevant accounts: Scrutinising financial information, including the company’s ability to settle debts, its financial position, knowledge of subsequent events, and consideration of future liabilities.

- Articles: Complying with any additional requirements set forth in the company’s articles.

- Dividend policy: Examining the existence and adherence to a dividend policy.

- Class rights: Checking for different classes of shares and rights attached to certain classes.

- Shareholders’ agreement: Examining the relevant clauses within the shareholders’ agreement that address the procedures for shareholder voting in approving a final dividend and ascertaining the presence of an incorporated dividend policy.

- Directors’ duties: Ensuring compliance with directors’ duties, particularly under section 172 CA 2006.

Shareholder approval for interim payments

While an ordinary resolution is a requirement for final dividends, shareholder approval for interim dividends hinges on the company’s articles and dividend policy. It is important to check whether payments in specie is permitted at all.

- Dividends in specie: Without express authority in the company`s articles, it cannot make distributions in specie. The company is obliged to pay all the dividends in cash. Over and above the authority, some articles normally state that directors` authority to pay dividends in specie is generally subject to shareholder approval via ordinary resolution. The Model articles grant express authority to pay all, or a part of a dividend or other distributions owed in relation to a share through the transfer of non-cash assets of equivalent value (article 34(1)).

- Distribution in specie: Technically a distribution in specie does not need an ordinary resolution, unless it falls under substantial property transactions (“SPT”) in accordance with section 190 CA 2006. Please see this case study for more information on SPT.

What are unlawful dividends and rectification?

An unlawful dividend occurs when a company lacks sufficient distributable reserves to cover the amount of distribution. The consequences of an unlawful dividend include the following:

- The company is in violation of CA 2006 by paying the unlawful dividend.

- Directors are in breach of their duties unless the error was reasonable and honest. Directors may be required to repay the dividend or compensate the company for any resulting loss. Additional complications may arise if the company enters insolvency, potentially leading to reverse transactions which are proven to be transactions at undervalue, transactions defrauding creditors, or transactions at preference.

- Recipient shareholders may be obligated to repay the dividend if they were aware or should have been aware of its unlawfulness.

Typical reasons of unlawful dividends include having sufficient distributable profits that are not disclosed in annual accounts and the absence of interim account preparation. Additionally, group-related issues, like relying on a dividend or reduction by a subsidiary that is considered invalid, and other accounting challenges, such as problems with asset valuation, can contribute to the occurrence of unlawful dividends.

Unlawful dividends cannot be rectified through ratification. In practice, companies may replace the unlawful dividend by declaring a release and issuing a new dividend. Concerning directors, the breach of director’s duty cannot be ratified by the company or shareholders, but a resolution can potentially release the directors from responsibility. Shareholders may repay the unlawful dividend, release it, or treat it as a shareholder’s loan.

How our corporate solicitors can help

In summary, successfully navigating the legal complexities of dividends necessitates a thorough grasp of company law and a detailed understanding of the particulars of each situation and the individual company involved. At Moore Barlow, we stand ready to assist you with any concerns or inquiries related to dividends, whether you are a director or a shareholder.